.svg)

.svg)

.svg)

.svg)

.svg)

.svg)

.svg)

.svg)

.svg)

.svg)

.svg)

.svg)

Minimum Wage: The statutory minimum wage in France is typically €12.02 EUR per hour, amounting to ~€1,443.11 EUR per month for a typical 35 hour work week.

Working Hours: Employers in France must adhere to strict labor laws that regulate working hours, overtime, and employee rights.

Payroll Taxes: In France, employers are required to make payroll contributions that fund social security, health care, and other statutory employee benefits.

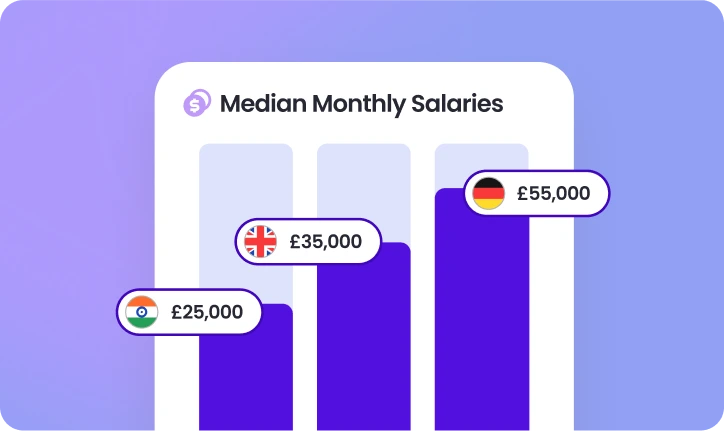

Average Salary: The average gross monthly salary in France is approximately €3,150–€3,350 (about USD 3,450–3,650) as of early 2026.

Hiring independent contractors has boomed in popularity because of the cost savings and flexibility they offer. It can be a great option if you require niche skills or short-term project support. Contractors allow businesses to access specialized skills quickly, without the time and cost of setting up a local entity.

However, it’s important to know the limits of this model: contractors are not a substitute for full-time employees. Relying on them for ongoing, long-term roles can create serious compliance risks, including employee misclassification, which can lead to fines, back taxes, and reputational damage.

Playroll’s contractor management solutions make it simple to compliantly engage, onboard, and pay contractors around the world. We provide clear visibility into agreements, streamline payments, and reduce compliance risks – so you can focus on getting the work done. And when you’re ready to take the next step, we can help seamlessly convert contractors into full-time employees through our global Employer of Record service.

From compliant contracts to competitive benefits, Playroll’s EOR services keep you aligned with local labor laws and regulations, safeguarding your business, so you can focus on growth.

Book a Demo

Businesses can only operate smoothly in France if they comply with local labor laws including drafting compliant employment contract agreements and meeting taxation and payroll obligations. Learn more about the employment laws and regulations in France below, to avoid any compliance issues.

Employment Contract Requirements

France follows European Directive 2019/1152, requiring employers to communicate key employment terms in writing. Employment contracts, whether permanent or fixed-term, must be in French, regardless of the employee's language proficiency. The following formalities must be followed when employing in France:

- Filling out pre-hiring declaration by the employer (“déclaration préalable à l’embauche”)

- Informing the French Labor Administration of the employment (“Inspection du travail”)

- Registering company with complementary pension funds

- Acquiring health insurance and provident insurance in compliance with French law and applicable collective bargaining agreements

- Recording full names of employees in the staff register (“registre du personnel”)

- Completing immigration formalities for non-French employees (excluding European nationals)

Onboarding Process

We can help you get a new employee started in France quickly, with a minimum onboarding time of just 1-2 working days. The timeline starts once the employee submits all required information onto the Playroll platform and completes any necessary local authority registrations. For non-nationals, the Right to Work assessment (if applicable) may add up to three extra days. Additional time may be needed for follow-ups on this assessment. Please note, payroll cut-off dates can impact the actual start date. Playroll's payroll cut-off date is the 10th of each month unless otherwise specified.

In France, the average gross monthly salary in early 2026 is around €3,150–€3,350 (about USD 3,450–3,650), which you can use as a benchmark as you budget for your team. Actual pay varies significantly by experience, industry, and location, with information technology, finance and banking, and pharmaceuticals typically offering higher wages than retail or hospitality. Salaries in major cities such as Paris, Lyon, and Marseille are generally above the national average, so your company may need to offer higher pay in these urban centres to attract and retain talent.

As of early 2026, annual inflation in France is running at roughly 2–3%, while real GDP growth for 2025–2026 is projected at about 1–1.5% and the unemployment rate is around 7–7.5%. For your company, this combination of moderate inflation and modest growth means you can plan relatively stable wage increases without extreme cost pressures. At the same time, a mid‑single‑digit unemployment rate still provides a reasonably broad pool of candidates for your openings, especially outside the tightest labour markets in major cities.

Employers in France must adhere to strict labor laws that regulate working hours, overtime, and employee rights. The standard workweek is 35 hours, with a maximum daily limit of 10 hours and a weekly cap of 48 hours. Industry-specific exceptions and managerial roles may follow different rules, often outlined in collective agreements. Employees are entitled to minimum rest periods, including 11 consecutive hours daily and 35 consecutive hours weekly. Night and weekend work are subject to additional regulations, often requiring special authorization or enhanced compensation.

Overtime is tightly controlled, with a legal limit of 220 hours per year per employee. Employers must compensate overtime at 125% of the regular wage for the first eight additional hours (36th to 43rd hour) and 150% beyond that. Non-compliance with working hour and overtime regulations can lead to legal penalties, fines, and potential criminal charges. To maintain compliance, employers should carefully track employee hours, adhere to rest requirements, and ensure proper overtime compensation.

A flat-rate deduction of €0.50 per overtime hour has been introduced for companies with 50 to 249 employees.

As of 2026, France’s minimum wage – known as the Salaire Minimum Interprofessionnel de Croissance (SMIC) – is set at €12.02 per hour (gross). This corresponds to a gross monthly salary of €1,823.03 for full-time employees working the standard 35-hour workweek. After social contributions, the net monthly wage is estimated at approximately €1,443.11.

The SMIC applies universally, including to expatriates, ensuring equal minimum pay across the workforce. However, certain exceptions exist. Apprentices and young workers may receive a reduced percentage of the SMIC depending on age and experience, while interns are not paid a salary but instead receive a legally defined financial compensation (gratification minimale).

The French minimum wage is reviewed annually on January 1 and may also be adjusted mid-year if inflation exceeds 2 percent. The SMIC is indexed to inflation and broader economic conditions to help protect workers’ purchasing power. In addition, collective bargaining agreements in some industries may set higher minimum wages based on skill level, qualifications, or job responsibilities. Employers in France must stay informed of these updates to ensure compliance with labor laws and fair compensation practices.

Global expansion shouldn't mean losing time to paperwork or dealing with complicated, country-specific HR systems. An Employer of Record helps you keep your focus on talent by handling the operational side of employment in France. That includes onboarding, contract management, payroll processing, and statutory compliance, all aligned with local laws and best practices. The EOR guarantees that employees are legally employed and properly supported from day one.

This streamlined setup allows you to prioritize recruiting the best people and integrating them into your company culture. Your team stays lean, and you avoid getting caught up in the details of local processes or shifting regulations. For founders, global hiring managers, or HR teams working across borders, an EOR multiplies your impact, reducing admin time, preventing errors, and helping ensure that new hires have a smooth experience from the get-go.

Employer Tax Contributions

Employer payroll contributions are generally estimated at an additional 40% to 45% on top of the employee salary in France.

Employee Payroll Tax Contributions

In France, the typical estimation for employee payroll contributions cost is around 22% to 25%.

Individual Income Tax Contributions

Income tax is computed using progressive rates in France, reaching up to 45%. Factors like household status and the number of children can impact the overall tax rates.

Pension in France

In France, pension eligibility requires at least 10 years of residence and work in the country, with 40-43 years of employment for the maximum pension. Supplementary and private pension plans are also available. The retirement pension, administered by French Social Security, can be claimed at age 62, offering between 37.5% and 50% of the average annual income over a 25-year career.

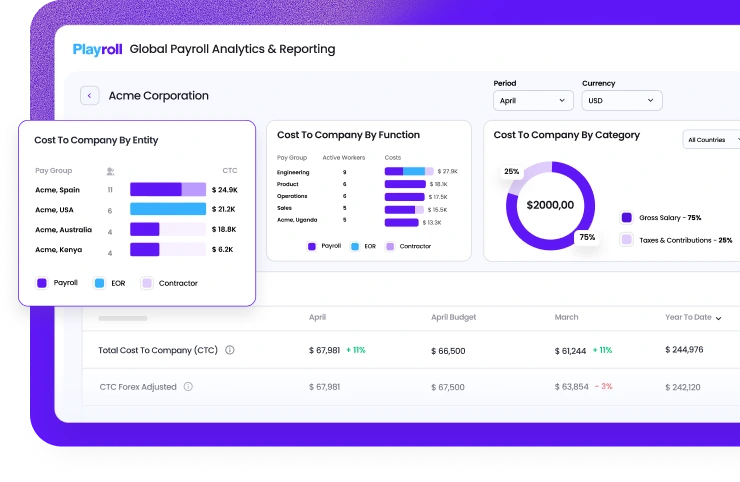

Employers in France must navigate a complex payroll system that includes income tax withholding, social security contributions, and other levies, each with specific rates and deadlines.

Non-compliance can lead to significant penalties and strained employee relations. Implementing payroll management software can streamline these processes, ensuring accurate calculations and timely submissions, thereby helping employers consolidate payroll data and maintain compliance with French regulations.

Hiring in France means taking on local payroll obligations, which often include unique tax rates, contribution rules, and strict documentation. If you're not familiar with the system, or don't have a local entity, it’s easy to make mistakes. That’s where an Employer of Record ccomes in. The EOR manages payroll for your team on your behalf, ensuring every process is accurate, timely, and legally compliant.

Key Ways an EOR Supports Payroll in France:

- Full Legal Compliance: Ensures all payments, deductions, and filings meet country-specific requirements.

- Payroll Setup & Processing: Handles salary calculations, tax withholdings, and local reporting obligations.

- Statutory Benefit Contributions: Pays into required social programs and manages country-mandated benefits.

- Employee Documentation: Generates compliant contracts and manages hiring and termination paperwork.

- Local Currency Payouts: Delivers salaries in local currency, avoiding delays or exchange rate issues for employees.

Make better business decisions by consolidating global payroll data, while seamlessly syncing your existing payroll operations.

Book a Demo

France requires most non-EU/EEA/Swiss nationals to hold both a suitable long-stay visa (visa de long séjour) and an accompanying work authorization, such as the titre de séjour "salarié" or "passeport talent" (Talent Passport). In practice, the employer usually initiates the work authorization with the French authorities, and the employee then applies for the corresponding visa at the French consulate in their country of residence.

Key routes for skilled workers include the Passeport Talent (for highly qualified employees, intra‑company transferees, researchers, and certain tech or startup profiles), the standard salarié work permit for local hires, and the salarié détaché for seconded workers. Each route has specific salary thresholds, qualification criteria, and documentation requirements, and compliance with French labor law and social security rules is central to a successful application.

Mandatory Leave Entitlement in France

The annual leave entitlement in France is 25 days for a full time worker. These can include public holidays on top of that or within those days, which would otherwise be unpaid.

Public Holidays In France

France observes 11 public holidays mandated by law, which are separate from the minimum holiday entitlement in the French Labor Code. The Alsace region and the Moselle department observe two extra days. Employers usually grant these public holidays as days off, and collective bargaining agreements specify that employees must take time off on these days:

Paid Time Off in France

As per France's labour code, employees are entitled to a minimum of five weeks of paid vacation annually, granted after completing one month of probation, in addition to public holidays. However, it is customary to allocate extra leave days through collective bargaining agreements.

Maternity Leave In France

Maternity leave lasts 16 weeks for the 1st or 2nd child (6 weeks before the due date, 10 weeks after birth), extendable for third or subsequent children, and much longer for multiple births (twins, triplets). The leave may also be extended in cases of medical complications.

To receive maternity pay from Social Security, the employee must have been affiliated for 10 months before the due date, and also have worked at least 150 hours during the 90 days prior to the start of leave (or contributed equivalent in other cases). Payment is based on the average salary over the three months preceding the start of the leave, subject to a social security ceiling/cap. Allowances are paid every 14 days.

Paternity Leave

Paternity leave lasts 28 calendar days (35 in case of multiple births). The first 3 working days after birth are paid by the employer, followed by 25 calendar days covered by social security. Of this, 4 consecutive days must be taken immediately after the birth, and the remaining 21 days can be used within 6 months, either consecutively or split into two periods of at least 5 days. Multiple births add 7 extra days. Eligibility generally requires notifying the employer at least one month in advance. Payment is based on the average daily salary over the last 3 months, subject to a social security cap.

Sick Leave In France

Employees with over three months of service and 150 hours worked are entitled to unlimited paid sick leave based on their regular salary. They must provide a medical certificate to the employer within 48 hours to obtain a Social Security salary certificate. The first three days serve as a qualifying period, and from the fourth day onward, Social Security covers the pay. Additional compensation from the employer is detailed in collective or company agreements.

Parental Leave In France

Employees with at least one year of service at their child’s birth may request up to one year of unpaid parental leave, renewable twice up to a maximum of three years, or switch to part-time (pro-rata) with employer approval. A monthly PreParE allowance is available, subject to prior insurance contributions, with extended support for those with multiple children. In addition, parents can take 3–5 days’ leave for a child’s illness, with extensions possible depending on the child’s age and medical condition.

Bereavement Leave

If an employee experiences the loss of an immediate family member, they are entitled to three days of leave.

Adoption Leave

In the case of adopting a child that involves travel, employees can take six weeks of unpaid leave.

France has comprehensive leave policies designed to protect employees' rights while ensuring workplace productivity. Full-time employees are entitled to a minimum of 30 working days of paid annual leave per year, accrued at 2.5 days per month worked.

This entitlement is separate from the 11 national public holidays, which may be granted as additional time off depending on company policies. Employers must ensure compliance with these regulations and allow employees to take their accrued leave within the legal timeframe.

In addition to annual leave, France mandates various other types of leave, including sick leave, which requires a medical certificate and is partially compensated by Social Security. Maternity leave lasts 16 weeks, with potential extensions for multiple children, while paternity leave allows for 28 days off. Employees can also take parental leave for up to three years, either full-time or part-time. Special leave options such as family solidarity leave and sabbaticals are also available under specific conditions.

To ensure compliance with French labor laws, employers must implement clear leave policies, track employee leave balances accurately, and promote a healthy work-life balance by encouraging employees to take their entitled leave.

In France, employers are legally required to provide several key benefits to employees, including health insurance, pension plans, life and disability insurance, paid annual leave, maternity and paternity leave, sick leave, work injury insurance, unemployment insurance, public transportation reimbursement, and regular medical examinations.

Beyond these mandatory provisions, many employers offer supplemental benefits to attract and retain top talent. These may include supplementary health insurance, additional retirement plans, enhanced life and disability coverage, extra paid leave, extended parental leave, supplementary sick leave benefits, comprehensive accident insurance, income protection plans, company cars or transportation allowances, and wellness programs.

It's essential for employers to understand and comply with these legal requirements while considering additional benefits to support employee well-being and remain competitive in the job market.

When hiring across multiple countries, maintaining consistency in how you deliver employee benefits quickly gets tricky. Each country, including France, has its own legal rules, cultural norms, and contribution systems. An Employer of Record helps you strike the right balance between global structure and local compliance. They take over the complexity of delivering benefits that are aligned with France’s legal requirements and competitive with local market expectations.

From ensuring statutory benefits are in place to managing local onboarding timelines and enrollment systems, the EOR provides a seamless experience for both employer and employee. This makes it easier to grow your team across borders without reinventing your benefits process in each new location. You stay in control of your overall benefits strategy, while the EOR takes care of executing it in a way that works legally and culturally in France. It’s a smarter way to scale benefits globally without losing local relevance.

In France, employment termination is strictly regulated, requiring a "real and serious cause" for dismissal. Employers can terminate employees on personal grounds, such as misconduct or professional incompetence, or economic grounds, including financial difficulties and company restructuring. The termination process involves a mandatory preliminary meeting, a decision period, and a formal notification of dismissal. Notice periods range from one to three months based on the employee's tenure, except in cases of gross misconduct where no notice is required.

Severance pay is mandatory for employees with at least eight months of service, calculated based on tenure and salary. Additional compensation may be granted under collective bargaining agreements. French labor laws provide strong protections against unfair dismissal, allowing employees to challenge terminations in labor courts, which may result in reinstatement or financial compensation. Employers must also provide final pay settlements and essential termination documents, ensuring compliance with legal obligations.

Termination Process in France

Employment agreements can be concluded through redundancy, resignation, or mutual agreement negotiation. However, termination due to COVID-19 is prohibited in France. To formally end the employment, employers must provide the employee with the following documents:

- Position certificate ("certificat de travail")

- A document for the French Public Employment Service ("Pôle emploi") for unemployment benefits

- Employer statement on owed amounts ("solde de tout compte")

Notice Period in France

In France, notice periods, including post-probationary periods, extend based on the duration of employment:

- 0-6 months of service: determined by relevant collective agreements (ranging from 24 hours to 30 days)

- 6 months-2 years of service: 1 month notice

- 2 years above: 2 months' notice

- For executives: 3 months' notice

Severance in France

Mandatory severance payments are required for dismissals, contract breaches, or mutual termination in France. The amount is typically calculated based on the highest figure among the monthly average over the past year, the general monthly average, or one-third of the payment over the last three months. It varies depending on the employee's seniority:

- First 10 years of seniority: 1/4 of monthly salary per year

- After 10 years of seniority: 1/3 of monthly salary per year

Disclaimer

THIS CONTENT IS FOR INFORMATIONAL PURPOSES ONLY AND DOES NOT CONSTITUTE LEGAL OR TAX ADVICE. You should always consult with and rely on your own legal and/or tax advisor(s). Playroll does not provide legal or tax advice. The information is general and not tailored to a specific company or workforce and does not reflect Playroll’s product delivery in any given jurisdiction. Playroll makes no representations or warranties concerning the accuracy, completeness, or timeliness of this information and shall have no liability arising out of or in connection with it, including any loss caused by use of, or reliance on, the information.

ABOUT THE AUTHOR

Jayde De Wet

Jayde is an experienced Research Associate at Playroll, a leading Employer of Record (EOR) provider. Jayde has a strong background in legal compliance, data analysis and market research, specializing in identifying emerging trends and driving innovation in global HR solutions.

.svg)

.png)

.webp)

.svg)