.svg)

.svg)

.svg)

.svg)

.svg)

.svg)

.svg)

.svg)

.svg)

.svg)

.svg)

.svg)

Hiring employees in the Netherlands means understanding a highly regulated, employee-protective labor system with strict rules on contracts, working hours, and dismissals. From your very first hire, you’re expected to comply with Dutch Civil Code Book 7 and any applicable collective labour agreement (CAO), and issue a written employment contract from day one detailing probation (up to a maximum of two months), salary, hours, and notice.

You must also apply the statutory minimum wage, withhold and remit wage tax and social security contributions to the Belastingdienst (with an employer share of approximately 20–30%), handle holiday pay (at least four weeks plus an 8% allowance), and register for payroll obligations. When it comes to termination, even probation offers limited flexibility. Most dismissals require prior UWV approval or court permission for a reasonable ground, plus transition payments (severance) after 2 years, or you risk unfair dismissal claims and potential reinstatement.

If you don’t have a local entity, the compliance burden can escalate quickly with tax residency risks and strict social security rules. In this guide, we’ll walk you through exactly what you need to set up payroll correctly, structure contracts properly, manage statutory entitlements, and avoid early mistakes that lead to penalties or employee claims.

Minimum Wage: The statutory minimum wage in The Netherlands is typically 14.71 EUR per hour, amounting to ~2,550.00 EUR per month for a typical 40 hour work week.

Working Hours: In the Netherlands, employers must adhere to strict regulations regarding working hours and overtime to ensure compliance and protect employee well-being.

Payroll Taxes: In The Netherlands, employers are required to make payroll contributions that fund social security, health care, and other statutory employee benefits.

Average Salary: The average gross monthly salary in The Netherlands is approximately €3,600–€3,900 (about USD 3,900–4,200) as of early 2026.

How To Hire Employees In The Netherlands

Hiring in The Netherlands for the first time can be overwhelming, especially when navigating unfamiliar employment laws. So, how do you get started? There are three main ways to hire in The Netherlands: set up your own legal entity, hire independent contractors, or use an EOR service to handle payroll and global HR for you. Below, we’ll walk you through each option in detail.

1. Set Up A Local Entity In The Netherlands

Setting up a local entity in The Netherlands is the traditional route for businesses that want to build a long-term presence in a new market. It allows for direct hiring, fine control over operations, and compliance with local labor laws.

That said, the process is rarely simple. It involves navigating complex legal structures, extensive registration procedures, ongoing payroll administration, and local tax obligations. Beyond the administrative burden, the costs of incorporation, maintaining local offices, and hiring compliance experts can quickly add up.

For companies operating with slim margins or testing new markets, these financial and operational commitments often make setting up a local entity an unfeasible option compared to more flexible and cost-effective solutions.

2. Use an Employer of Record in the Netherlands

If you want to hire in the Netherlands without setting up a local entity, an Employer of Record (EOR) can act as the legal employer of your team in the Netherlands. They handle everything from payroll to ensuring compliance with Dutch employment law, tax rules, and social security obligations. This allows you to move quickly while ensuring your employment arrangements align with the Netherlands’ protective labor laws from day one.

While the Netherlands doesn’t have a blanket joint employer statute, courts can find shared liability in triangular setups if your company exerts significant control over the work or integrates the employee deeply into your organisation. This can extend exposure for issues like unfair dismissal, wage claims, or discrimination complaints to your business. It’s important to partner with an EOR that has strong local expertise so contracts are robust, responsibilities are clearly defined, and your risk exposure is minimized.

Cost of Employer of Record vs Setting Up an Entity

If you’re deciding between setting up a Dutch entity or using an EOR, ask yourself two questions: how many employees are you hiring, and how much risk and administration are you willing to take on?

Setting up your own entity (for example, a BV) involves government fees of approximately €50–500 for incorporation via the Chamber of Commerce. However, foreign companies typically spend €10,000–40,000 or more upfront on legal, notary, tax, and advisory support to register properly, obtain a VAT number, open payroll accounts, and ensure full compliance from the outset.

Ongoing costs then include:

- Accounting, bookkeeping, and payroll support: Often €1,000–4,000 or more per month

- Annual filings, corporate tax returns, and social security declarations

- Internal time managing Belastingdienst remittances, wage tax submissions, jaaropgave statements, and compliance processes

- Full exposure to UWV procedures, court disputes, or unfair dismissal claims (including transition payments and potential reinstatement)

With an Employer of Record, you skip incorporation entirely. EOR fees in the Netherlands typically range from €300–€800 or more per employee per month (most commonly €500–700 for standard services), depending on the provider, employee seniority, benefits administration, and additional services such as CAO compliance. There’s no entity to maintain, no local director requirements, no separate tax infrastructure to build, and significantly lower risk of missteps with flexible work reforms or permanent establishment issues.

3. Hire Independent Contractors In The Netherlands

Hiring independent contractors has boomed in popularity because of the cost savings and flexibility they offer. It can be a great option if you require niche skills or short-term project support. Contractors allow businesses to access specialized skills quickly, without the time and cost of setting up a local entity.

However, it’s important to know the limits of this model: contractors are not a substitute for full-time employees. Relying on them for ongoing, long-term roles can create serious compliance risks, including employee misclassification, which can lead to fines, back taxes, and reputational damage.

Playroll’s contractor management solutionsmake it simple to compliantly engage, onboard, and pay contractors around the world. We provide clear visibility into agreements, streamline payments, and reduce compliance risks – so you can focus on getting the work done. And when you’re ready to take the next step, we can help seamlessly convert contractors into full-time employees through our global Employer of Record service.

From compliant contracts to competitive benefits, Playroll’s EOR services keep you aligned with local labor laws and regulations, safeguarding your business, so you can focus on growth.

Book a Demo

Businesses can only operate smoothly in The Netherlands if they comply with local labor laws including drafting compliant employment contract agreements and meeting taxation and payroll obligations. Learn more about the employment laws and regulations in The Netherlands below, to avoid any compliance issues.

Employment Contract Requirements

While written employment contracts are not obligatory for legal validity in the Netherlands, it is advisable for employers to provide essential details about the job to their employees within the initial month. In accordance with Dutch Civil Code, employers are required to communicate the following information to the employee:

- Identification and details of both parties

- Job title and job description

- Starting date (and duration for temporary contracts)

- Base salary and payment terms, including: compensation, benefits, and pension schemes (if applicable)

- Daily or weekly working hours

- Leave entitlements and number of holidays

- Probation period

- Notice for employment termination

- Collective labour agreements

- Non-competition clause (if applicable)

Onboarding Process

We can help you get a new employee started in The Netherlands quickly, with a minimum onboarding time of just 1-2 working days. The timeline starts once the employee submits all required information onto the Playroll platform and completes any necessary local authority registrations.

For non-nationals, the Right to Work assessment (if applicable) may add up to three extra days. Additional time may be needed for follow-ups on this assessment. Please note, payroll cut-off dates can impact the actual start date. Playroll's payroll cut-off date is the 10th of each month unless otherwise specified.

In The Netherlands, the average gross monthly salary in early 2026 is around €3,600–€3,900 (about USD 3,900–4,200), which serves as a practical benchmark as you budget for your team. Actual pay varies significantly by experience level, industry, and location, with information technology, finance and banking, and specialized manufacturing typically offering higher wages. You can expect to pay more in major urban centres such as Amsterdam, Rotterdam, The Hague, and Utrecht, where competition for talent is stronger and wages for your employees tend to be above the national average.

Macroeconomic conditions in The Netherlands are relatively stable, with inflation in late 2025 and early 2026 hovering around 2–3%, which helps you plan predictable wage increases for your workforce. Real GDP growth is projected at roughly 1.5–2.0% for 2025–2026, supporting steady but not rapid expansion in labour demand. Unemployment is low at about 3–4%, meaning your company faces a relatively tight labour market and may need to offer competitive salaries and benefits to attract and retain qualified employees.

In the Netherlands, employers must adhere to strict regulations regarding working hours and overtime to ensure compliance and protect employee well-being. Employees aged 18 and over are allowed to work up to 12 hours per day and 60 hours per week, but these are exceptional limits. Over a 16-week period, the average workweek should not exceed 48 hours. Full-time employment typically ranges from 36 to 40 hours per week, though the Netherlands has one of the shortest average work weeks in the world at 29 hours. Overtime compensation is not mandated by law but should be clearly defined in the employment contract or collective labor agreements (CAOs). Many employers establish rates at either 50% or 100% of the regular pay for overtime work, or time off in lieu.

Employers must also ensure adequate rest periods, including 11 consecutive hours of daily rest and 36 consecutive hours of weekly rest. Night shifts and weekend work are subject to specific rules, and employees are entitled to a break during long shifts.

As of January 1, 2026, the statutory minimum wage in the Netherlands is:

- €14.71 per hour for employees aged 21 and older.

- This amounts to €2,550.00 per month for a typical 40 hour work week.

The Dutch government adjusts the minimum wage biannually, on January 1 and July 1, to reflect economic conditions such as inflation and wage growth. The minimum wage applies to all employees, including full-time and part-time workers, with younger employees receiving a percentage of the adult rate based on their age.

Additionally, specific rules apply to interns, trainees, and expatriates. While internships tied to educational programs may be unpaid, those performing regular work must receive at least the statutory minimum wage.

Expats are generally subject to the same minimum wage laws, although highly skilled migrants may have higher salary thresholds. Various factors, such as industry-specific variations and government policies, influence wage levels as well.

Hiring in the Netherlands puts you in a system where employee protections are robust, dismissals need solid justification and external approval in most cases, and recent 2026 changes have phased out zero-hour contracts while boosting security for flexible workers. One wrong step and you could face UWV rejection or even court challenges.

A properly structured EOR becomes the legal employer in the Netherlands, managing the compliance framework so you avoid direct exposure while focusing on your team’s output.

Your EOR partner should handle:

- Drafting compliant employment contracts aligned with Dutch law and any applicable CAO

- Assisting with compiling the correct documentation for successful registration with the Belastingdienst for wage tax and social security, remitting contributions

- Running monthly payroll, issuing compliant payslips, and preparing jaaropgave

- Administering statutory entitlements: minimum wage (~€14.71/hour for 21+ as of 2026), overtime rules, holiday pay (4+ weeks + 8% allowance), public holidays, and various leaves

- Ensuring proper onboarding/offboarding to reduce risks of disputes or unfair dismissal exposure

- Maintaining records and handling ongoing filings

You keep full control of day-to-day direction and performance. The EOR carries the legal and administrative load. If you’re hiring one or two people to test the market (a developer in Amsterdam, a marketer in Rotterdam, etc.), scaling slowly, or avoiding CAO complexities, an EOR gives you speed, serious risk reduction, and cost certainty without the overhead and learning curve of setting up an entity.

Employer Tax Contributions

Employer payroll contributions are generally estimated at an additional 24.84%-36.3% on top of the employee salary in The Netherlands.

Employee Payroll Tax Contributions

In The Netherlands , an employee's social security contributions are included in income tax deductions.

Individual Income Tax Contributions

The individual tax rate in the Netherlands is calculated based on progressive rates and can vary from 35.82% to 49.50%.

Pension in The Netherlands

The retirement age in the Netherlands is currently 67 years but is scheduled to increase to 67 years and 3 months in 2028 according to life expectancy. Employees insured for 50 years are eligible to receive full government pension (AOW), which is paid monthly and adjusted twice a year based on wage inflation.

Employees can also choose supplementary pension plans, known as the Second Pillar Pension, with about 90% of employers offering to provide extra financial support alongside AOW.

Employers in the Netherlands must manage various payroll taxes, including wage tax, social security contributions, and employee insurance contributions, all of which are critical for compliance with Dutch regulations. Wage tax is progressive, requiring precise calculations based on employee income, while social security and employee insurance contributions fund essential programs such as pensions and disability benefits.

Timely filing and remittance of these taxes are essential to avoid penalties, with monthly deadlines applying to most tax types. Monthly payroll taxes must be filed by the last day of the month following the pay period. Setting up payroll requires registration with the Dutch Tax and Customs Administration, and employers must stay updated on current rates and rules to ensure accuracy. Using payroll management software can simplify tax calculations, consolidate payroll data, and ensure compliance with Dutch tax regulations, reducing administrative burdens and improving efficiency.

One of the biggest risks in global hiring is payroll mismanagement. In The Netherlands, even small errors in tax reporting or social contribution payments can trigger audits, fines, or reputational damage. For companies without in-country expertise, the risk isn’t worth taking. An Employer of Record removes this burden by owning the legal responsibility of payroll, executing every step with built-in compliance.

Key Ways an EOR Supports Payroll in The Netherlands:

- Mitigates Compliance Risk: Oversees all legal obligations for payroll, tax filings, and recordkeeping.

- Local Regulatory Expertise: Interprets and applies The Netherlands’s latest labor and tax changes in real time.

- Free Processing: Reduces mistakes in wage calculations and reporting through built

- Payroll Record Management: Maintains compliant payroll audit trails and documentation for each employee.

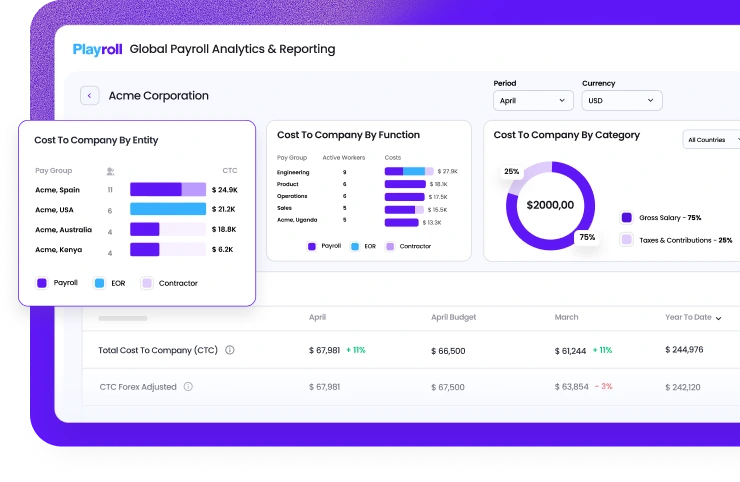

Make better business decisions by consolidating global payroll data, while seamlessly syncing your existing payroll operations.

Book a Demo

In the Netherlands, most non-EU/EEA and non-Swiss nationals need authorization to live and work, typically through a combination of a residence permit and a work authorization linked to a specific employer. Common routes include the highly skilled migrant permit (kennismigrant), the EU Blue Card, the Intra-Corporate Transferee (ICT) permit, and the Single Permit (gecombineerde vergunning voor verblijf en arbeid, GVVA), which combines residence and work authorization in one.

Employers usually act as sponsors and must be recognized by the Dutch Immigration and Naturalisation Service (IND) for many knowledge-migrant and fast-track options. The Dutch Employee Insurance Agency (UWV) may be involved in assessing labor market conditions for certain permits. Processing times vary by permit type, but careful preparation, complete documentation, and using recognized sponsorship routes can significantly streamline the process for both employers and employees.

Mandatory Leave Entitlement in The Netherlands

The annual leave entitlement in The Netherlands is 20 days for a full time worker. These can include public holidays on top of that or within those days, which would otherwise be unpaid.

Public Holidays In The Netherlands

The Netherlands has 11 public holidays, which are not part of the minimum paid leave entitlement. Nevertheless, employers typically grant their employees time off on these public holidays. The following are the nationally recognised holidays in the Netherlands:

Paid Time Off in The Netherlands

A full-time employee in the Netherlands receives 20 days of paid annual leave each year, and this can be increased to anything between 25 and 32 days.

Any statutory leave from the previous year must be utilized by the end of June of the following year, and the employer is obligated to inform the employee of its expiration. Non-statutory leave expires after 5 years.

Maternity Leave In The Netherlands

Pregnant employees are entitled to 16 weeks of paid maternity leave (generally 6 weeks before and 10 weeks after), which includes a compulsory 4-week leave period. The employer covers this leave at 100% of the employee's daily wage. In the case of multiple births, the paid maternity leave is extended to 20 weeks.

If the employee remains unable to work due to pregnancy or childbirth, the maternity leave can be prolonged. Employers initially make the payment and later seek reimbursement through the UWV. Maternity leave typically consists of two periods:

- Prenatal Leave: The employee is required to take 4-6 weeks of leave before the expected due date.

- Postnatal Leave: The remaining 10-12 weeks must be taken after the child's birth, allowing the employee to rest.

Paternity Leave In The Netherlands

The spouse or partner of an employee who recently gave birth gets 1 week of paid 'birth leave' to be taken within the first four weeks after childbirth. This is paid at 100% by the employer. They also have the right to take 'short absence leave' for the actual birth.

Additionally, they can take an Extended Partner Leave for 5 weeks within the first six months after the child's birth. During this extended leave, they are eligible to receive compensation of up to 70% of their last earned salary from the UWV.

Sick Leave In The Netherlands

If an employee is unable to work due to illness, the employer must provide compensation of at least 70% of their last earned salary, including holiday allowance, for a duration of 2 years. This is often outlined in employment contracts with details such as:

- The employer will pay 70% or 100% of the employee's full salary (the amount is not capped) for the 1st year of illness

- The employer will pay 70% of the employee's salary (the amount can be capped) during the 2nd year of illness

Parental Leave In The Netherlands

Parents with children under 8 years old are eligible for parental leave of 26 times their weekly working hours. The initial 9 weeks are paid by the UWV at 70% of their usual salary and should be taken within the first year of the child's life. The subsequent 17 weeks are unpaid.

This arrangement can be negotiated and distributed over the 8-year period, with leave allocated for each child.

Adoption Leave

Parents intending to adopt or foster a child are entitled to a maximum of 6 weeks of leave. This leave can be taken in a continuous period or distributed over the initial 26 weeks after the child arrives at their home. A notice of 3 weeks must be given before taking this leave, and during this time, adoption allowance can be applied for through the UWV.

Care Leave

Employees can opt for leave to care for an ailing family member through three provisions: Emergency Leave, a one-day, paid leave for unforeseen urgent matters; Short-term Care Leave, allowing up to double the weekly working time for 2 weeks, with the employer covering 70% of their salary; and Long-term Care Leave, offering up to six times the weekly working time for 6 weeks, albeit unpaid.

In the Netherlands, employees are entitled to a minimum of 20 days of paid annual leave per year, separate from public holidays, which are typically unpaid unless stated in contracts. Employers must ensure statutory leave is taken within six months of the following year, and employees receive a holiday allowance of at least 8% of their annual salary.

Other mandatory leave includes sick leave (up to 104 weeks at 70% pay), maternity leave (at least 16 weeks with full salary via social security), and paternity/partner leave (1 week at full pay, plus 5 additional weeks at 70% pay). Parental leave grants 26 times the weekly working hours per child, with 9 weeks being partially paid at 70% of regular wages up to a maximum of 297,82 euros per day. Employers must comply with these laws to ensure fair treatment and effective workforce management.

In the Netherlands, employers are legally required to provide several key benefits to employees, including a minimum wage, paid time off, holiday allowance, paid sick leave, and parental leave.

To attract and retain top talent, many employers also offer supplemental benefits such as pension plans, additional health insurance, performance bonuses, transportation allowances, and professional development opportunities. Understanding and implementing these benefits, while adhering to legal requirements, are crucial for employers aiming to foster a supportive and competitive work environment.

In The Netherlands, benefits play a central role in attracting and retaining top talent. Employees often expect more than just a paycheck – they're looking for stability, healthcare coverage, pension plans, and other perks that show a company is invested in their well-being. If you're not familiar with what’s standard or required, you risk falling short. An Employer of Record helps bridge that gap by administering a locally competitive benefits package that meets both legal requirements and employee expectations.

An EOR doesn't just check boxes, they make sure your employees receive benefits that are timely, properly communicated, and well-managed from the moment they’re onboarded. From managing healthcare contributions to adjusting for regional differences in leave or bonus entitlements, an EOR acts as both a legal and operational partner. The result is a better employee experience, less administrative burden on your internal team, and greater confidence that your offer is aligned with what top candidates in The Netherlands actually want and need.

In the Netherlands, employment termination is strictly regulated, requiring employers to have valid legal grounds and follow proper procedures. Dismissal may be based on economic reasons, underperformance, long-term illness, or serious misconduct. Employers must generally obtain approval from the Employee Insurance Agency (UWV) or the subdistrict court before proceeding with termination, except in cases of mutual agreement or during probationary periods. Notice periods range from one to four months, depending on the employee's length of service (less than five years: one month; 5-10 years: two months; 10-15 years: three months; more than 15 years: four months), though immediate dismissal is allowed in cases of gross misconduct.

Employees are often entitled to severance pay, known as the transition payment, which equals one-third of their monthly salary per year of service, capped at €98,000 or one year's salary if higher. Employers must also provide final pay, including wages, bonuses, and compensation for unused leave. Dutch labor law protects employees against unfair dismissal, allowing them to challenge terminations that lack a valid legal basis. Proper documentation, such as termination letters and final payslips, must be provided to ensure compliance with legal obligations.

Termination Process in The Netherlands

An employer in the Netherlands has the authority to terminate an employment agreement with a valid reason, as specified in both the employment agreement and any collective agreement in place with the employee. However, unilateral termination without involving the Employee Insurance Agency (UWV) is not permissible, particularly in cases related to economic reasons or long-term disabilities. According to Dutch law, valid reasons for termination include:

- Redundancy due to economic circumstances

- Long-term disability (lasting two years)

- Frequent absence due to illness or disability affecting the ability to carry out job duties

- Underperformance

- Misconduct

- Refusal to fulfill contractual duties based on conscientious or religious objections

- A disturbed relationship

- Other grounds than those mentioned above

- Cumulated dismissal grounds based on more than two dismissal grounds combined

Notice Period in The Netherlands

In the Netherlands, when termination occurs through mutual agreement, securing the employee's consent involves following notice periods. These periods take place at the end of the month and are based on the employee's length of service:

- Less than 5 years: 1 month notice

- Between 5-10 years: 2 months notice

- Between 10-15 years: 3 months notice

- More than 15 years: 4 months notice

Severance in The Netherlands

Statutory severance payment is due when the employment agreement is terminated and is determined based on the following:

- 1/3 of salary per year worked. Severance pay is capped at the higher of 98000 EUR and 1 years' salary.

- A transition payment becomes applicable where employer initiates the dismissal, and the employee is not blameworthy.

Disclaimer

THIS CONTENT IS FOR INFORMATIONAL PURPOSES ONLY AND DOES NOT CONSTITUTE LEGAL OR TAX ADVICE. You should always consult with and rely on your own legal and/or tax advisor(s). Playroll does not provide legal or tax advice. The information is general and not tailored to a specific company or workforce and does not reflect Playroll’s product delivery in any given jurisdiction. Playroll makes no representations or warranties concerning the accuracy, completeness, or timeliness of this information and shall have no liability arising out of or in connection with it, including any loss caused by use of, or reliance on, the information.

ABOUT THE AUTHOR

Jesse Weisz

Jesse is an experienced R&D Analyst at Playroll, a leading Employer of Record (EOR) provider. With a strong background in data analysis and market research, Jesse specializes in identifying emerging trends and driving innovation in global HR solutions. She is an all-rounder, critical thinker and success-seeker (often inextricably linked to being a late-night tea drinker).

.svg)

.png)

.webp)

.svg)